South Korea’s Economy Accelerates Despite the Middle East Energy Shock

Despite South Korea’s heavy reliance on Middle Eastern energy, its GDP growth projection in 2026 is among the highest in the world.

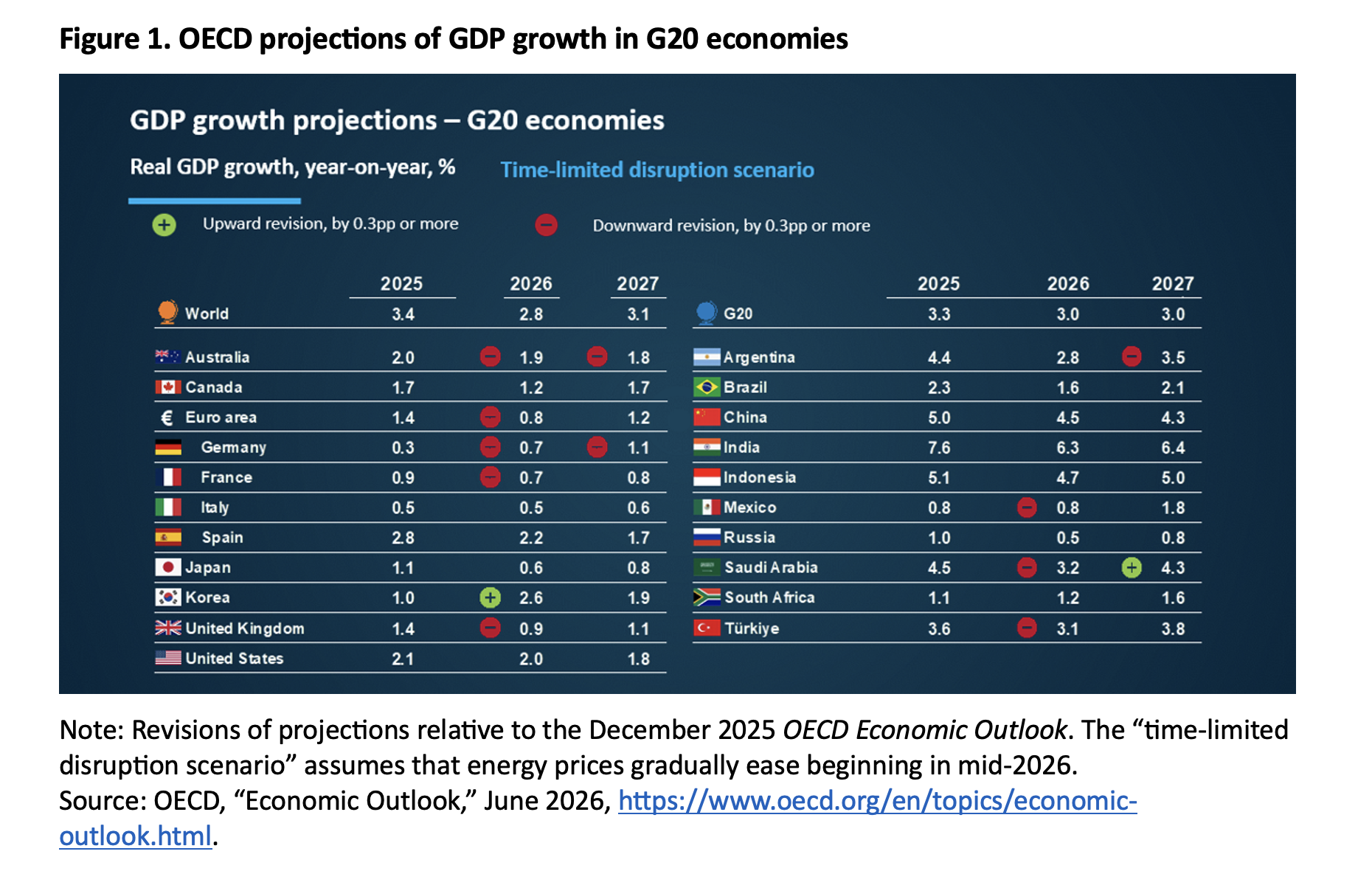

War in the Middle East has cut the global growth outlook. However, despite South Korea’s heavy reliance on Middle Eastern energy, the OECD Economic Outlook in June 2026 raised the country’s 2026 growth projection to 2.6 percent from 1.0 percent in 2025, the only upward revision among Group of Twenty (G20) economies. An AI-driven boom sent Korea’s semiconductor exports surging nearly 170 percent in May. Chips now make up some 42 percent of Korean exports, leaving export growth heavily dependent on one industry just as cars, machinery, and steel all contracted in May.

At the beginning of 2026, global growth prospects were poised for a significant upward revision, thanks to strong investment in AI, supportive financial conditions, and easing trade tensions. But the June 2026 OECD Economic Outlook projects that world GDP growth would slow from 3.4 percent in 2025 to 2.8 percent in 2026, assuming that energy prices gradually ease beginning in mid-2026 (Figure 1). World GDP in 2026 would slow to only 2.1 percent if the conflict persists to 2027.

Accelerating Growth in 2026

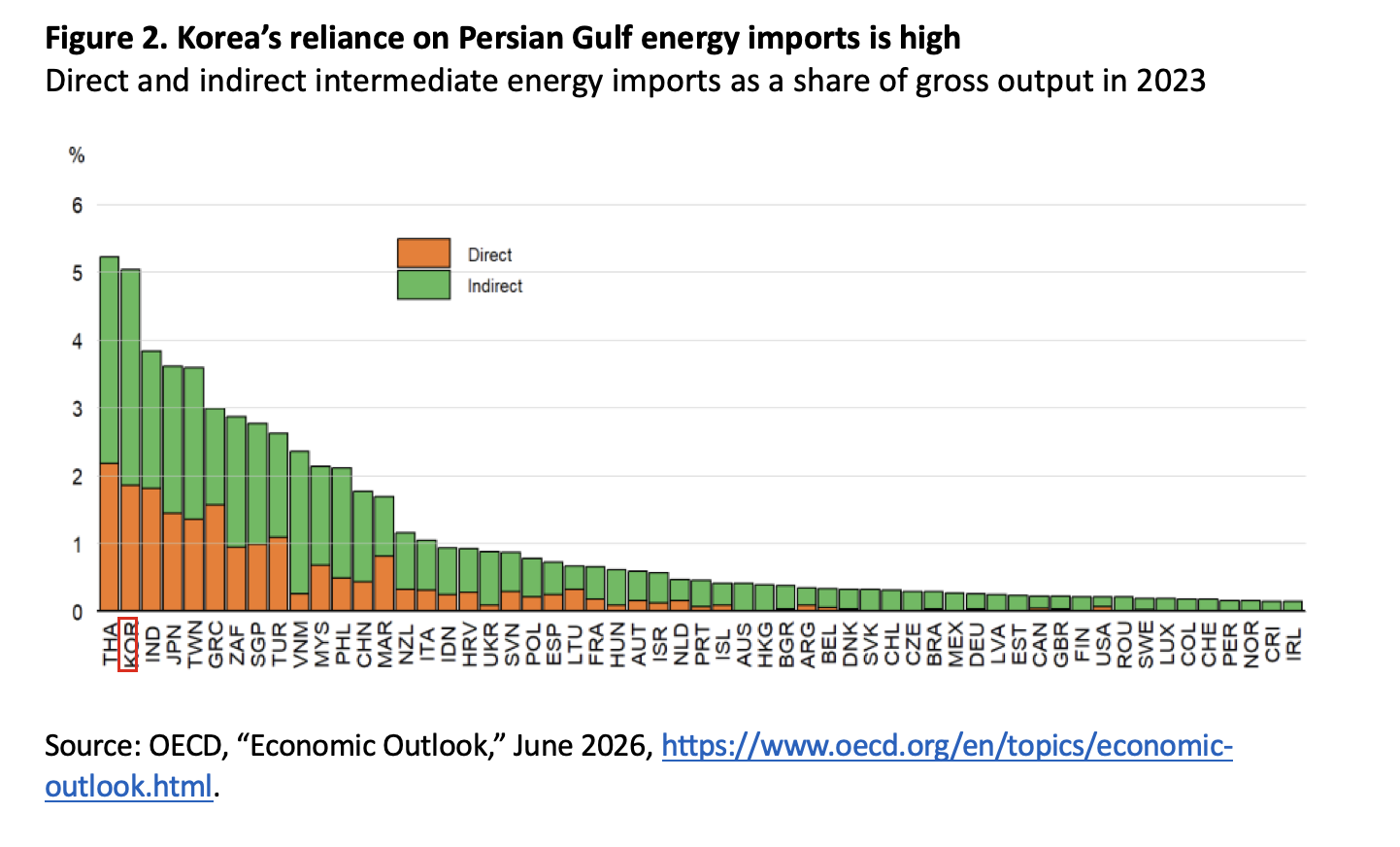

Korea’s direct and indirect intermediate energy imports from the Persian Gulf amounted to 5 percent of the country’s gross output in 2023, the highest among OECD countries (Figure 2). This contributed to the downgrading of Korea’s growth projection from 2.1 percent in December 2025 to 1.7 percent in the March 2026 OECD Economic Outlook, Interim Report. However, the impact thus far has been mitigated by Korea’s large strategic crude oil inventory, which is the world’s seventh-largest.

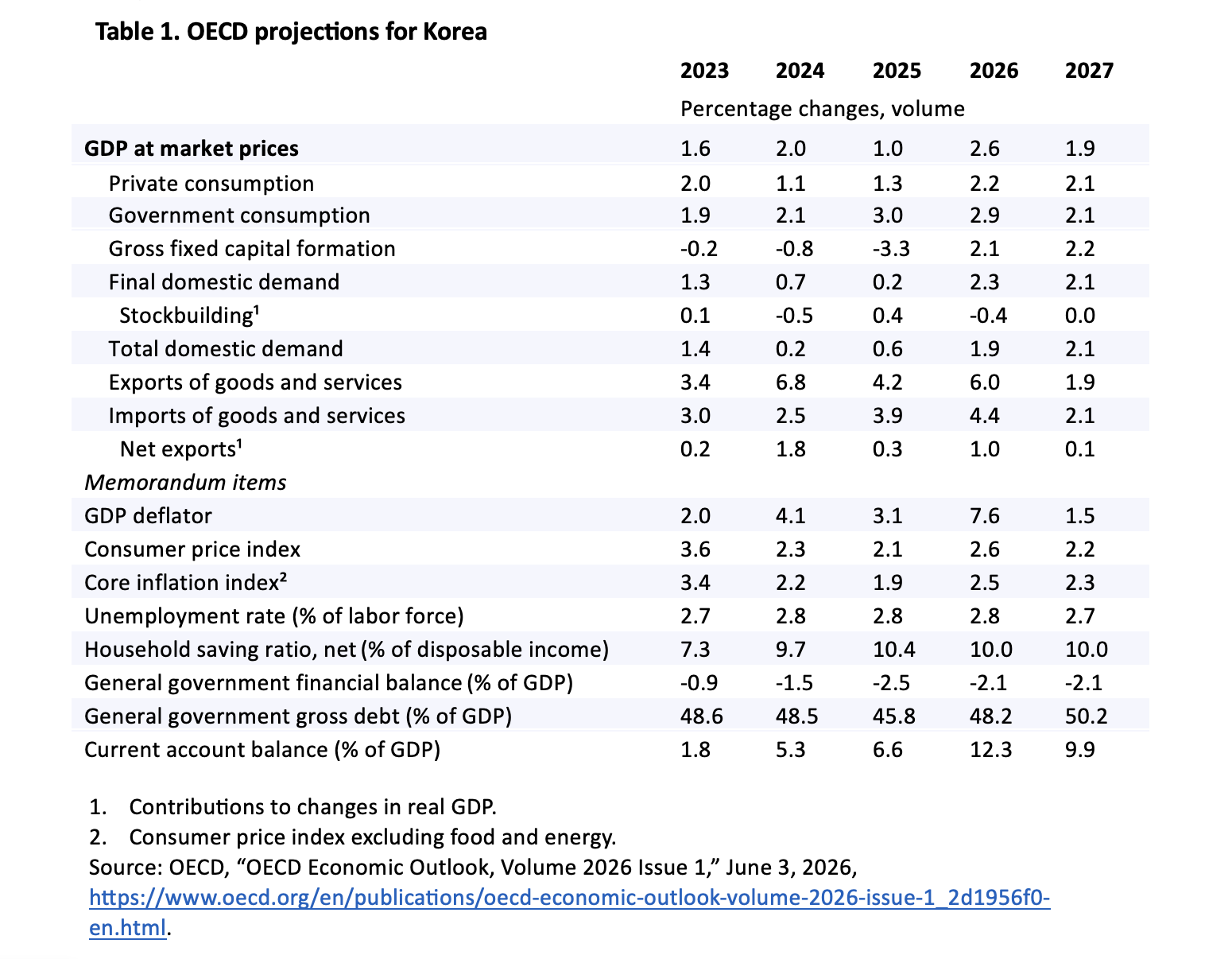

Korea’s GDP growth is now projected to pick up from 1.0 percent in 2025 to 2.6 percent in 2026 (Table 1). Korea is the only G20 country and one of only two OECD countries (along with Denmark) with at least a 0.3 percentage-point increase in its GDP growth projection for 2026 relative to the December 2025 OECD Economic Outlook (Figure 1). The OECD projection for 2026 tracks with estimates from the Korea Development Institute (2.5 percent) and the Bank of Korea (2.6 percent).

After a decline in the final quarter of 2025, Korea’s GDP rose 1.7 percent (quarter-on-quarter) in the first three months of 2026, the largest quarterly increase since 2020. Robust growth continued into the second quarter, with May exports rising 53.2 percent compared with the same month in 2025. Semiconductors are driving export growth, increasing 169.4 percent year-on-year to its highest monthly figure ever, reflecting surging worldwide investment in AI. Other information-technology products, such as computers, also achieved large gains. Net exports are projected to account for 1.0 percentage point of the expected 2.6 percent rise in GDP in 2026. The current account surplus is expected to exceed 12 percent of GDP (Table 1), its highest level ever and far above the 1.3 percent recorded in 2022.

Buoyant export growth and the stock market reaching record highs in early June have helped improve business confidence. These factors are expected to help reverse the decline in gross fixed capital formation over 2023–2025, with growth of around 2 percent in 2026 (Table 1).

The favorable economic trends have also boosted private consumption, which is projected to surpass 2 percent in 2026 for the first time since 2022 (Table 1). In addition, government measures aimed at offsetting the supply shocks from the Middle East conflict have had a positive impact. The April supplementary budget of KRW 26.2 trillion (USD 17.7 billion), more than 1 percent of GDP, is helping households, businesses, and local governments cope with the impact of the high energy costs and supply chain disruptions. In March, the government implemented price controls on key petroleum products and reduced taxes on gasoline and diesel by 15 percent and 25 percent, respectively.

But reducing the price of energy products weakens incentives to save energy and achieve greenhouse gas emission reduction targets. Further, the benefits are universally available. Targeting support on vulnerable households and firms would provide effective protection at a lower fiscal cost, which is important for medium-term fiscal sustainability. As energy prices normalize, support should be phased out. In sum, measures to mitigate the impact of higher energy prices on households and firms should be targeted and temporary, while preserving incentives to reduce energy use.

Rising Inflation

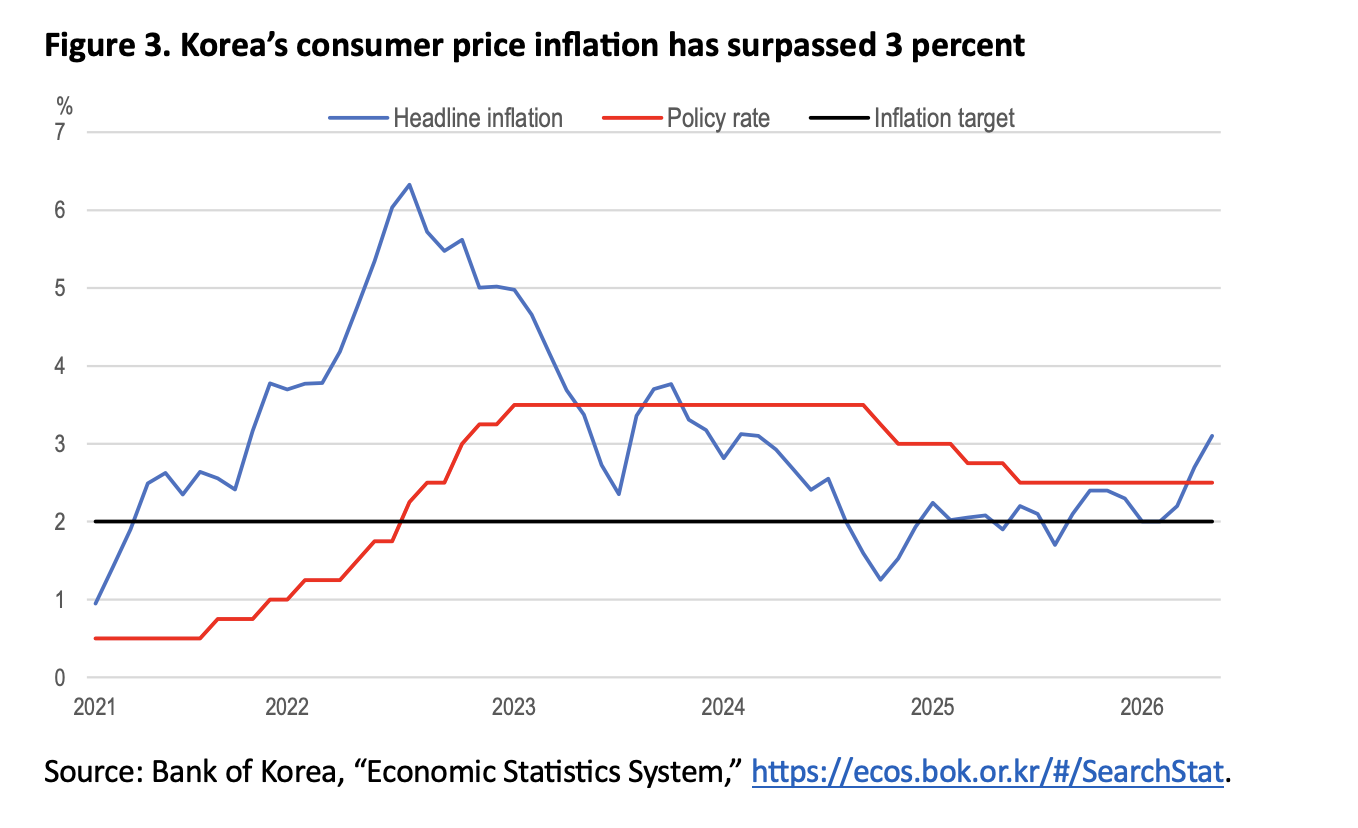

Consumer price inflation, which had been steady at 2 percent in early 2026, rose to 3.1 percent in May (Figure 3). Core inflation, which excludes food and energy prices, has been more stable, rising to 2.5 percent in May, matching its rate in February. The OECD projects that headline inflation will reach 2.6 percent in 2026, while the Bank of Korea expects 2.7 percent.

At its May 28 Monetary Policy Board meeting, Korea’s central bank kept its policy (base) rate unchanged at 2.5 percent—the rate set a year ago. As a general rule, monetary policy should remain focused on anchoring inflation expectations while “looking through” temporary supply shocks. The bank stated that “given the uncertainties surrounding developments in the Middle East and that their spillover effects remain high, the Board judged that it would be appropriate to maintain the current level of the base rate.”

Conclusion

The Korean economy faces both upside and downside risks related to developments in the Middle East, changes in the world trading system, and the pace of semiconductor sector expansion and its spillover effects on domestic demand. Korea’s increasing dependence on semiconductor exports, which accounted for 42.3 percent of total exports in May, and on other information-technology sectors may leave it vulnerable to negative shocks in those industries.

Meanwhile, exports of other manufactures declined in May, including cars (down 5.9 percent), home appliances (down 21.7 percent), general machinery (down 6.3 percent), and steel (down 2.1 percent). Inflation is another concern, and higher interest rates may be necessary to anchor inflation expectations.

The policy response to the energy price shock should prioritize targeted support to vulnerable households and businesses. Phasing out energy price ceilings, fuel tax cuts, and export controls would improve energy efficiency and reduce fiscal pressures. Fiscal deficits have become persistent in recent years, while spending pressures related to population aging are set to intensify. A framework that aligns annual budgets with a sustainable long-term fiscal trajectory is essential. The OECD suggests a cyclically adjusted net lending limit and the designation of an independent fiscal institution to monitor compliance. Another priority is to improve spending efficiency.

Randall S. Jones is a Distinguished Fellow at the Korea Economic Institute of America (KEI). The views expressed here are the author’s alone.

This material is distributed by KEI on behalf of the Korea Institute for International Economic Policy. Additional information is available at the Department of Justice, Washington, DC.